Buying your first home in Cambridge is exciting, but it can also feel daunting. Prices here sit above the national average, competition for the best homes is real, and the process has more moving parts than most people expect. The good news is that with the right preparation you can approach it with confidence. Here is a clear, practical guide to getting onto the Cambridge property ladder.

Before you fall in love with a listing, get your finances straight. The average price paid by first-time buyers in Cambridge was around £394,000 in early 2026, a little lower than a year earlier, so accurate budgeting matters.

Start with three numbers: your deposit, your borrowing capacity and your monthly outgoings. Most lenders want at least a 5–10% deposit, though a larger one unlocks better interest rates. Speaking to an independent mortgage adviser early is invaluable — they will tell you what you can borrow, what your repayments would look like, and which lenders suit your circumstances.

An agreement in principle (sometimes called a decision in principle) is a statement from a lender indicating how much they would likely lend you. It is not a guarantee, but it shows sellers and agents that you are a serious, ready buyer. In a market where good homes attract several interested parties, that credibility can make the difference between your offer being accepted or overlooked.

The purchase price is only part of the picture. Budget for:

Knowing these figures upfront prevents nasty surprises and keeps your budget realistic.

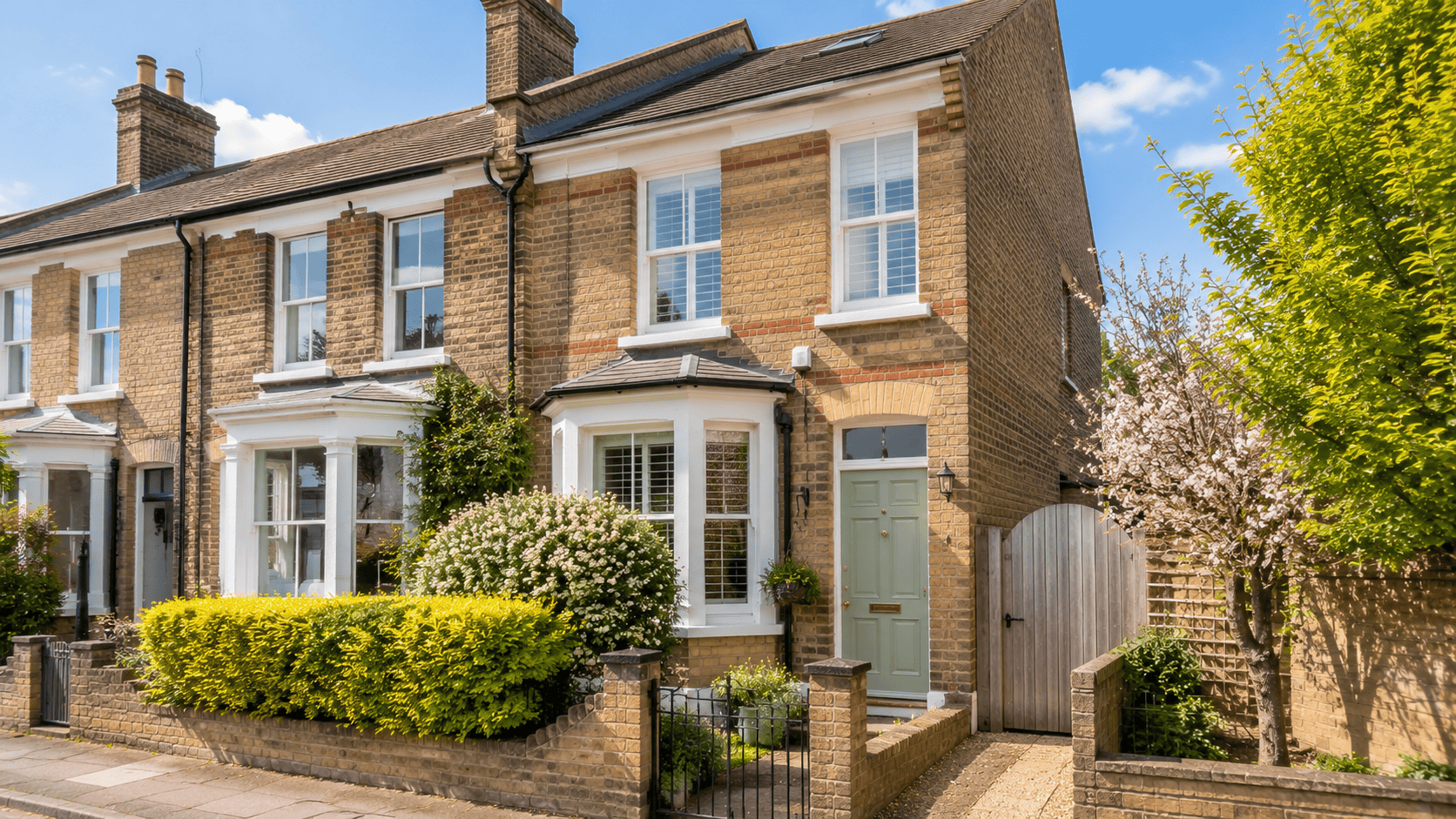

Cambridge rewards buyers who look beyond the obvious. Central neighbourhoods such as Romsey, Petersfield and Newnham carry a premium for their walkability and character. Push slightly further out and areas like Cherry Hinton, Trumpington and the growing Eddington and Darwin Green developments can offer more space for your money. The surrounding villages — Histon, Great Shelford, Sawston and beyond — add gardens, community and good schools within easy reach of the city.

Think about your daily reality: commute, schools, transport links and the lifestyle you want. The right compromise on location often unlocks a home you can actually afford.

When you find the right home, hesitation can cost you. Having your finances arranged, your solicitor briefed and your agreement in principle in hand means you can offer the moment it matters. At the same time, never let the pace pressure you into skipping a survey or overstretching your budget. A good agent will help you judge a fair offer and guide you through to completion.

Getting onto the Cambridge property ladder comes down to preparation: understand your budget, secure your mortgage position, account for every cost, and choose an area that fits both your life and your finances. Do that groundwork and you turn a stressful-sounding process into a manageable one. If you are starting your search, our team knows every corner of the Cambridge market and can help you find the right first home — and we offer independent mortgage advice to get you started.

Most lenders require at least 5–10% of the purchase price, but a larger deposit generally means a lower interest rate and wider choice of mortgage products.

Yes. First-time buyers benefit from relief up to set price thresholds. Because the rules and thresholds can change, confirm the current position with your solicitor or mortgage adviser before you budget.

It depends on your priorities. The city offers walkability and amenities at a premium, while villages and outer developments often provide more space and garden for the same money, with good transport links back into Cambridge.